The end of the Top 10 era: why The Winner Takes All is the new, brutal reality of AI search

Key takeaways

-

Language models (LLMs) compress traditional search results from a list of roughly ten links down to just one or two recommended brands - a reduction of over 80% in market visibility space.

-

Concentration is strongest in product and service categories with clear market leaders: finance, e-commerce, B2B software, and consumer electronics.

-

The LLM selection mechanism favors brands with high mention frequency across the web and structured, unambiguous data - not brands present in the greatest number of ranking positions.

-

The long-tail SEO strategy, built on traffic from positions 3–10, loses its economic justification in an AI Search environment, because users receive an answer before ever reaching the results list.

-

Generative Engine Optimization (GEO) - optimizing visibility in AI-generated responses - is becoming a fundamental dimension of brand monitoring, alongside traditional organic rankings.

-

The critical new metric is Share of Recommendations (a brand's share of generated recommendations) - an indicator unavailable in classical SEO tools.

-

Companies that do not measure their presence in AI responses are making budget decisions without knowing the real distribution of market attention.

From 10 links to just 2 answers: The scale of compression in AI Search

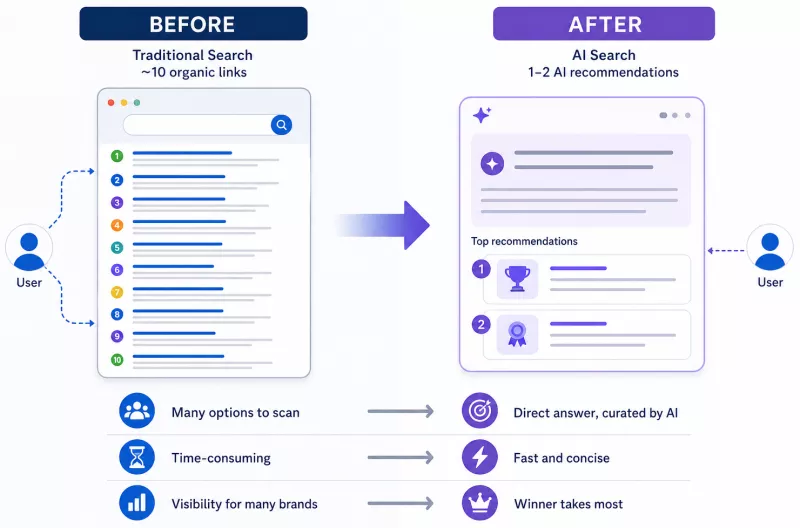

Search result compression is the transition from a multi-position list - historically around ten organic links on the first page - to a single, synthesized text response that names at most one or two brands. This is not a matter of interface style. It is a fundamental shift in who exists in the user's awareness at the moment of a purchasing decision.

A traditional Google search result created something like a democratic store shelf: first position had an advantage, but positions two through ten also generated traffic. Users scanned, compared, clicked. Today, when that same user poses a question to an AI assistant - whether in ChatGPT, Perplexity, Gemini, or the increasingly common AI Overview in Google - they receive an answer before they even see the list. And in that answer, there are typically two recommendations, not ten.

Data collected by the BrandInAI platform across thousands of queries shows that in categories with clear market leaders, the proportion of responses containing only one or two brands is significant. The dominant trend is toward a maximum of five recommendations, while displaying more applies to sectors with many leaders - such as food service (restaurant venues) across a larger geographic area - or cases where the user explicitly requests a greater number of options. The market for user attention has contracted, and with it the space in which a brand can exist at all.

How brand market visibility was measured

The BrandInAI analysis covered a representative sample of queries from product and service categories with high purchase value: B2B software (software as a service), consumer electronics, personal finance, e-commerce, and subscription services. Queries were formulated naturally - the way users actually ask them, not the way keyword phrases are constructed for SEO purposes. Each product category had a dozen or so queries covering different purchase intents.

The analysis window spanned three months of active monitoring. During that time, each query was tracked every day across several generative models (ChatGPT, Gemini, Claude, Perplexity). Brand visibility was defined as the brand being named explicitly in the generated response or in the recommendations section. A response was classified as containing one or two brands when a maximum of two names appeared in the main recommendation, regardless of any mentions later in the text. Results were aggregated at the category level rather than at the level of individual queries, which eliminates noise from random model variation and the tendency of a given query to return a specific number of results.

One important methodological limitation: AI models do not behave deterministically. The same phrase can produce a slightly different result on the next run. The figures presented in this article therefore rest on statistical aggregations, not individual samples. Every number cited here is supported by repeated tests.

Which industries are hit hardest by compression

The concentration of recommendations does not distribute evenly. It hits hardest in categories where users are seeking a specific product or service provider recommendation - and those categories are precisely the ones with the highest business stakes.

In B2B software, queries such as "best project management tool" or "marketing automation platform" consistently generate responses naming one to three brands. Beyond that group - silence. In consumer electronics, the pattern is similar: an AI assistant asked to recommend a laptop or wireless headphones names two or three options and stops. Users rarely ask further.

Consider the difference between a traditional supermarket and an expert-run shop. In the supermarket, the customer independently walks a forty-metre aisle. In the expert shop, they describe what they need and the salesperson hands them one item saying: "this is exactly what you need." AI Search operates like the second model - with the difference that the salesperson (the language model) has its own selection logic that cannot be changed by adjusting a cost-per-click bid.

This is not a market with a gentle gradient. It is a market with a cliff edge. A brand in fourth place does not receive four times less traffic than the first - it receives many times less, sometimes dozens of times less.

Why does artificial intelligence discard the surplus of information?

Language models are not search engines designed to present lists - they are response-generation systems. In that role, they function as ruthless content curators, prioritizing statistical certainty and consensus over exhaustive diversity. When a model must answer the question "which tool should I use," it optimizes for a response that will be perceived as helpful and credible - not for a response that is fair to every market participant.

From a business perspective, the logic is straightforward: the model selects brands about which it knows a great deal, consistently, and from multiple sources. Uncertainty is costly. If a model has repeatedly encountered positive, consistent mentions of brand A and sparse, scattered information about brand B, brand A is the safer choice for the model - even if brand B is objectively better for a specific use case.

The mechanism of aggregation and source authority building

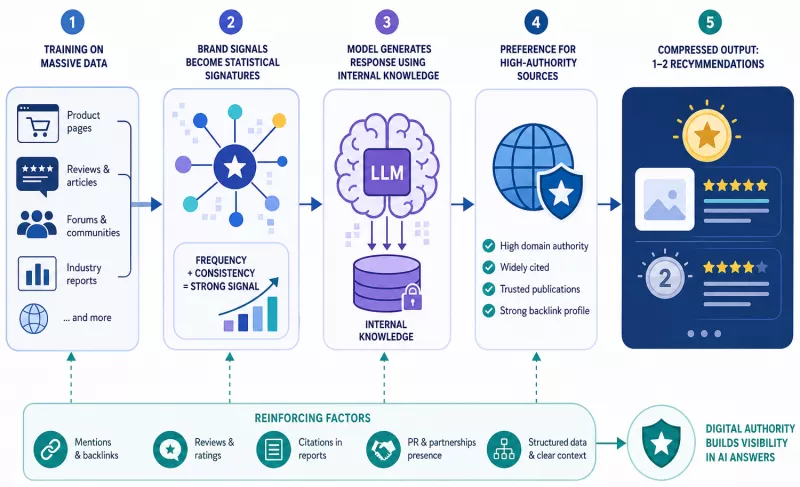

The way LLMs (large language models) arrive at recommendations can be outlined in a few steps, without going into the technical architecture.

First, the model was trained on a vast corpus of text from the internet - product pages, reviews, comparison articles, forums, and industry reports. In that process, brands with high mention frequency and consistency build a strong statistical profile in the model's parameters.

Second, when generating a response, the model does not search the internet in real time (unless it has a dedicated RAG module - retrieval-augmented generation - a mechanism that supplements knowledge by retrieving current documents). It draws on the knowledge encoded during training. Brands with a strong profile are, quite literally, more densely represented in that knowledge.

Third, even when the model has access to external sources (as in Perplexity or AI Overview), it favors sources with high domain authority - industry portals, widely read media outlets, pages with large numbers of citations. This amplifies the concentration effect: brands that were visible in prestigious places are rewarded twice over.

The outcome is predictable. A brand that has invested in broad web presence - links, mentions, reviews, citations in industry reports - has incomparably higher odds of appearing in a response than a brand that relied solely on keyword ranking positions.

The role of structured data and clear context

Simply being mentioned online is not enough. What matters is how a brand is described. Language models extract information easily from text that is organized, unambiguous, and free of marketing jargon.

A product page written in the style of "an innovative next-generation solution for dynamic enterprises" provides the model with very little usable information. A page that clearly defines: "a subscription management platform for SaaS companies, supporting integrations with Stripe and Chargebee, dedicated to finance and product teams" - provides concrete entities (precisely defined concepts and objects) that the model can associate with specific user queries.

Traditional SEO rewarded keyword density and text length. GEO rewards precision of definition, entity consistency, and the absence of ambiguity. This is a philosophical shift in content creation - from writing for a ranking algorithm to writing for a meaning-extraction algorithm.

Structured data (schema.org, FAQ markup, structured product descriptions) further enables models to retrieve information reliably and reproducibly. A brand that has invested in the machine readability of its content starts this competition from a stronger position.

The end of the long-tail era: Shifting traffic acquisition funnels

The business model built on free traffic from lower organic positions has been seriously disrupted. Data from the analyzed categories points to a strong, structural trend - though the scale and pace of this shift vary by industry and AI model.

For years, SEO rested on a diversified logic: the first position generates the most traffic, but positions three through ten also have value - especially for niche queries with clear purchase intent. A company could build a stable customer acquisition model on hundreds of long-tail phrases, each bringing a dozen visits per month but together forming a solid conversion stream.

Consider a mid-sized company offering software for physiotherapy practices. For years it attracted clients through phrases such as "national health fund billing software physiotherapy," "rehabilitation clinic management software," or "how to maintain a patient record in a physiotherapy practice." Users arriving through these phrases were highly motivated and close to a purchase decision. When AI Search starts answering those questions with a synthesized response that contains no link to this particular company, the stream dries up. In the analyzed categories, shifts of this kind occurred rapidly - often within weeks of AI Overview becoming widespread in a given query segment.

The invisibility of second-choice brands

The mechanism of brutal disconnection operates at the interface level. A user asks a question and receives an answer - and that answer occupies their entire attention. Even if a list of organic results appears below, the vast majority of users never reach it. Research into user behavior in AI Overview environments consistently shows a dramatic drop in CTR (click-through rate, the share of users who click a result) for results below the generated response.

Brands outside the narrow top tier of recommendations - say, a brand that historically held positions 4–7 - are entering a new era of near-complete invisibility. Not because their SEO has worsened. But because the interface space has shrunk to dimensions that fit two names, not seven.

The consequence is especially painful for niche and alternative products. The discovery of a new supplier by a user who did not previously know of its existence was one of the key values of organic search. AI Search, by responding synthetically, reduces that discovery space to a minimum.

The narrowing of niche queries and declines in organic SEO

Long-tail SEO rested on the assumption that users with very specific questions seek very specific answers and are willing to browse results in search of the best fit. That assumption is now being challenged by the behavior of AI systems.

When a user asks: "is it worth buying an ARM-processor ultrabook for remote work while travelling" - they used to land on comparison articles, reviews, and forum threads. They browsed, analyzed, decided. Today, ChatGPT or Perplexity give them an averaged but, in most cases, sufficiently good answer immediately. The smaller player whose detailed review held position six on Google loses that user before they even open a browser.

For expert sites, industry blogs, and niche publishers, this is an existential threat. Traffic generated by highly motivated users with precise intents - precisely those users with the highest conversion rates - is systematically migrating to AI interfaces, where the distribution of attention looks entirely different.

Budget shifts and the risk of market monopolization

For marketing directors and CMOs (chief marketing officers), the economics are straightforward and uncomfortable: a channel that was free or cheap for a decade now demands strategic reinvestment - but not in the form they are familiar with.

The defensive SEM (search engine marketing) strategy - buying keywords to defend against the loss of organic positions - loses effectiveness in an environment where users never see paid results because they stop at the generated response. Budgets previously spent on long-tail keyword campaigns must be at least partially redirected toward building brand digital authority - presence in prestigious publications, citeability in industry reports, and consistent brand narrative across dozens of external sources.

The systemic risk is serious. If the distribution of user attention concentrates on the recommendations of two or three AI platforms, and those platforms consistently promote the same two or three brands in every category, the market enters a self-reinforcing loop of monopolization. Brands at the top become progressively harder to displace, because their dominance is encoded in model training. This is not speculative forecasting - it is the logic that follows directly from the data aggregation mechanics described above.

New visibility metrics: What to measure in the AI Search era

Traditional keyword ranking reports - a brand at position 3 for phrase X, at position 7 for phrase Y - are no longer sufficient indicators of real market presence. A brand can hold excellent positions in a classical Google ranking while being simultaneously invisible in the environments where a growing number of users actually seek answers.

The need for continuous testing of AI model behavior follows directly from their non-deterministic nature. A model may recommend brand A today and, after an update or a change in query context, pass over it in silence tomorrow. Without systematic monitoring, these shifts are invisible to the marketing team until traffic declines grow large enough to appear in a financial report. Dedicated analytics platforms for measuring AI visibility - such as BrandInAI - are a reliable tool for tracking this new form of brand presence continuously and reproducibly, before the consequences become visible in sales figures.

Share of recommendations

Share of Recommendations is the percentage of AI-model-generated responses that include a brand's name, measured across queries in a given product or service category. If a brand appears in 40 out of 100 analyzed responses, its Share of Recommendations is 40%.

Why is this metric more important than keyword ranking position? Because it directly reflects how often an AI Search user heard a given brand named as a recommendation - not just how many times they had the technical option of clicking on it. In an environment where clicking is optional and the response is sufficient, exposure in a recommendation is the actual currency of visibility.

For business decision-makers, Share of Recommendations translates directly into an estimate of potential traffic from AI Search. A brand with a 5% share of recommendations in its category has a many times lower probability of generating new customer discoveries through the AI channel than a brand with a 40% share - regardless of its position in the traditional organic ranking.

Change detection and verification of technology partnerships

Share of Recommendations monitoring should be conducted regularly and cross-referenced with traditional organic traffic data. A correlation between a drop in AI recommendation share and a subsequent decline in organic CTR and direct visits may be the first signal that a shift in model behavior is already underway - before it reaches sales reports.

Companies should actively test whether their external activities - publications in industry media, content partnerships, participation in market reports - actually translate into growth of presence in AI responses. Links and media reach, which in the Google era were the currency of PageRank (the ranking algorithm based on the quality and number of links), are becoming, in the AI Search era, the currency of citeability and source authority in the model's judgment.

This requires a different way of thinking about media and publisher relations. It is no longer simply about an article in a prestigious outlet as PR (public relations). The point is that the article becomes a node in a network of cross-references that the model treats as a credibility signal. Verifying the effectiveness of these activities - at the level of management analytics, not just tooling - is becoming a standard of sound brand management in the AI era.

Summary: Brand strategy in a monopolized AI Search ecosystem

The compression of search results from ten links to one or two recommendations is not a passing technological curiosity. It is a structural shift in how users acquire information and make purchasing decisions - one that has already produced measurable consequences for the distribution of market attention.

The mechanics of this shift are logically consistent: LLMs aggregate knowledge from dozens of sources, prioritize brands with strong statistical profiles and unambiguous entities, and then present the user with one or two names instead of a list of ten options. The effect is merciless for everyone who fails to make it into that narrow group - and self-reinforcing for those who are already there.

The death of long-tail SEO is a consequence of this, not its cause. Niche phrases that for years built stable conversions for smaller players are losing value not because users have stopped searching for them. They are losing value because users receive an answer before reaching the results list - and that answer rarely names anyone outside the narrow front rank.

For decision-makers - marketing directors, heads of SEO/SEM, product managers - this analysis should be a signal to update priorities. Not to panic, but to conduct a precise review: which acquisition channels are already exposed to the risk of AI compression? What is the brand's current Share of Recommendations in its key categories? Are content and PR activities measured for their impact on visibility in AI-generated responses, not only on ranking positions?

These are questions worth asking today - while monitoring data on AI response visibility still allows for strategic choice and informed channel verification, rather than reactive crisis management.